Debt can feel like a heavy weight, affecting not only your finances but your emotional well-being. The journey to financial health after debt isn’t easy, but it’s achievable with a clear plan and practical strategies. In this guide, we’ll explore pro tips for rebuilding financial health, including the 75-15-15 and 50/30/20 rules, and strategies for financial recovery. Let’s dive in.

Understanding Your Financial Health Post-Debt: An Introduction

Debt can take a toll on every aspect of life. Once you’ve paid it off, you might feel relief mixed with uncertainty about what comes next. Rebuilding your financial health starts with acknowledging where you stand.

- Assess Your Financial Situation: Review your income, expenses, and savings. Online budget calculators can help you visualize your cash flow.

- Set Realistic Goals: Whether it’s saving for an emergency fund, investing, or planning for retirement, start small and work your way up.

To take control of your finances, explore free budgeting tools like Goodbudget or YNAB (You Need a Budget), which offer user-friendly ways to manage your money effectively.

Applying the 75-15-10 Rule: A Strategic Approach

The 75-15-15 rule is an effective framework for those recovering from debt:

- 75% for Essentials: Allocate 75% of your income to necessities like housing, food, and transportation.

- 15% for Savings: Build an emergency fund and start saving for future goals.

- 10% for Debt Repayment/Investments: If debt remains, dedicate 10% to tackling it. Once debt-free, channel this amount into investments.

This rule helps strike a balance between meeting current needs and preparing for the future.

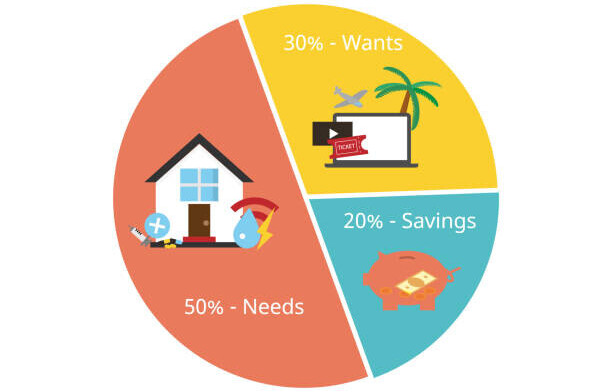

The 50/30/20 Rule: A Blueprint for Balanced Money Management

Another popular budgeting method is the 50/30/20 rule:

- 50% for Needs: Cover essentials like rent, groceries, and utilities.

- 30% for Wants: Allow room for discretionary spending, such as dining out or entertainment.

- 20% for Savings/Debt Repayment: Use this portion to save or accelerate debt repayment.

Adapt the percentages to suit your financial recovery plan. For instance, if you’re aggressively saving or paying off debt, consider adjusting to 60/20/20 or 70/10/20.

Steps to Reset Your Financial Life

A financial reset is vital for lasting stability. Here’s how:

- Declutter Your Financial History: Close unused accounts and streamline expenses.

- Create a New Budget: Use your preferred budgeting rule and stick to it.

- Build an Emergency Fund: Start with $500-$1,000 and gradually save 3-6 months’ worth of expenses.

Start building your financial safety net by using tools like this Emergency Fund Calculator.

Strategies to Get Out of Debt and Achieve Financial Stability

If lingering debt remains, prioritize these strategies:

- Debt Consolidation: Combine multiple debts into one for easier management.

- Snowball vs. Avalanche Methods: Choose between paying off the smallest debts first (snowball) or tackling high-interest ones (avalanche).

- Negotiate with Creditors: Request lower interest rates or payment plans.

Be consistent and track your progress. Each milestone will boost your confidence.

Take charge of your financial future with helpful guides on debt repayment strategies, like the Debt Snowball and Avalanche Methods available on Debt.org.

Building Sustainable Financial Habits

Healthy financial habits are the foundation of lasting stability:

- Track Spending: Use apps like PocketGuard to monitor daily expenses.

- Save Regularly: Automate transfers to your savings account.

- Embrace Affordable Living: Downsize where possible and seek cost-effective alternatives.

Remember, small changes compound over time.

Leveraging Resources and Tools for Continued Financial Growth

In today’s digital age, numerous resources can simplify financial management:

- Digital Apps: Use apps like Acorns for micro-investing or Credit Karma for credit score monitoring.

- Professional Advice: Consider consulting a financial advisor.

- Financial Education: Take online courses on platforms like Coursera or edX.

Stay informed and proactive to maintain financial health.

Rebuilding financial health after debt is a journey, but with the right strategies and tools, you can achieve stability and peace of mind. Start small, stay consistent, and watch your financial health flourish.